Chapter 8: Linear regression¶

8.4 Feature scaling via standard normalization¶

Press the button 'Toggle code' below to toggle code on and off for entire this presentation.

In [1]:

from IPython.display import display

from IPython.display import HTML

import IPython.core.display as di # Example: di.display_html('<h3>%s:</h3>' % str, raw=True)

# This line will hide code by default when the notebook is eåxported as HTML

di.display_html('<script>jQuery(function() {if (jQuery("body.notebook_app").length == 0) { jQuery(".input_area").toggle(); jQuery(".prompt").toggle();}});</script>', raw=True)

# This line will add a button to toggle visibility of code blocks, for use with the HTML export version

di.display_html('''<button onclick="jQuery('.input_area').toggle(); jQuery('.prompt').toggle();">Toggle code</button>''', raw=True)

8.4.1 Feature scaling for single input datasets¶

In [2]:

# load data

csvname = datapath + 'unnorm_linregress_data.csv'

data = np.loadtxt(csvname,delimiter = ',')

x = data[:,:-1].T

y = data[:,-1:]

# plot dataset

demo = regress_plotter.Visualizer(data)

demo.plot_data()

only two parameters to learn (the bias and slope of a best fit line)

let us take a look at its associated Least Squares cost function

In [4]:

# show the contours of an input function over a desired viewing range

static_plotter.two_input_contour_plot(least_squares,[],xmin = -12,xmax = 15,ymin = -5,ymax = 25,num_contours = 7,show_original = False)

- contours very elliptical

- these create a long narrow valley along the long axis of the ellipses

- as discussed in Section 6.4 gradient descent progresses quite slowly when applied to minimize a cost functions like this

- make a run of $100$ steps of gradient descent

In [6]:

# show run on contour plot

static_plotter.two_input_contour_plot(g,weight_history,xmin = -3,xmax = 7,ymin = -1,ymax = 12,num_contours = 7,show_original = False)

- little progress made in the long narrow valley of the function!

- the resulting fit is therefore quite poor

In [7]:

# the original data and best fit line learned from our gradient descent run

ind = np.argmin(cost_history)

least_weights = weight_history[ind]

demo.plot_fit(plotting_weights = [least_weights],colors = ['r'])

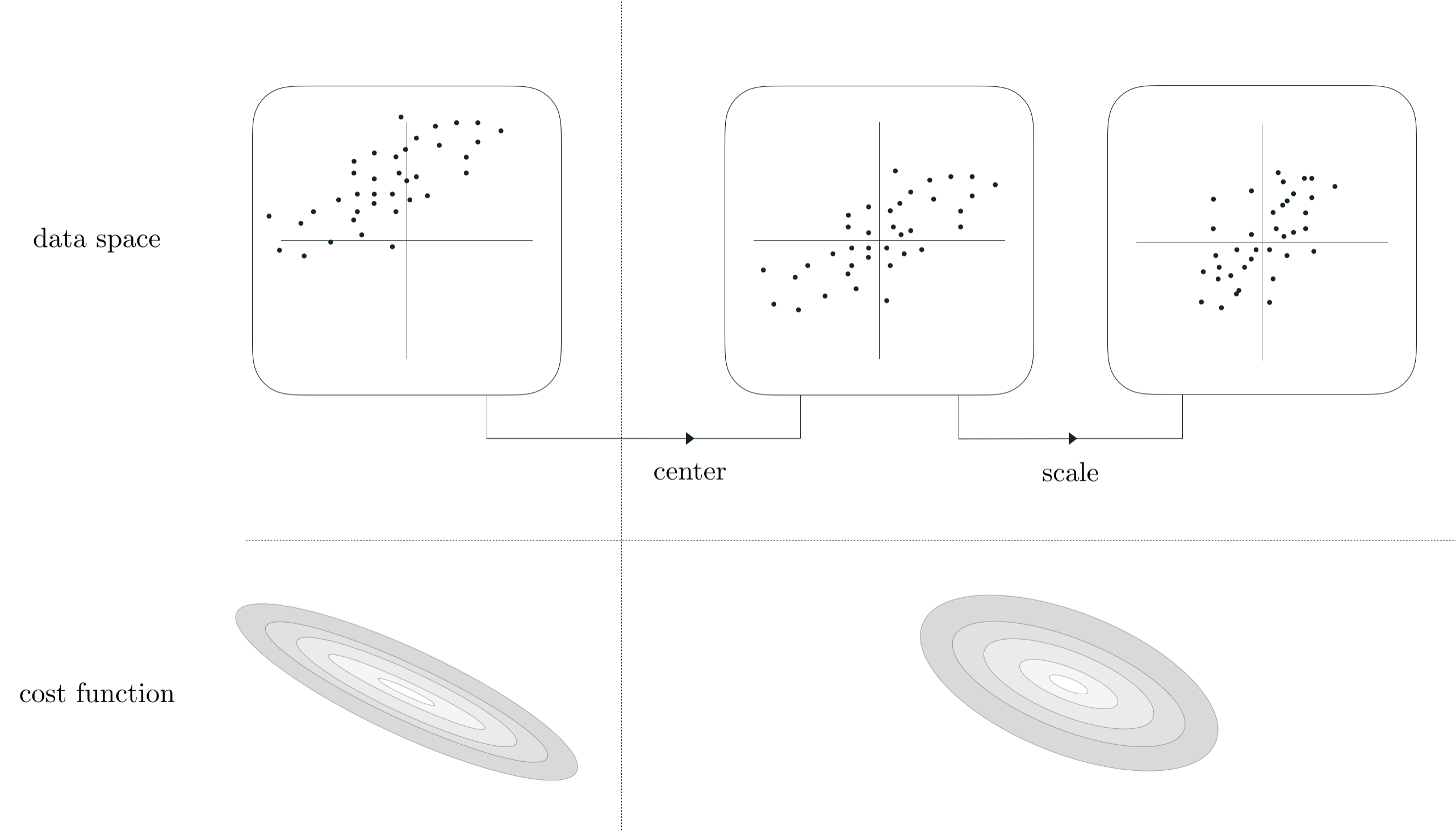

- an extremely simple adjustment of the data ameliorates this issue significantly, called standard normalization

- do the following to each input dimension / feature: subtract mean and divide off standard deviation

- for single input case, we replace each input $x_p$ point with its mean centered unit deviation analog as

where

\begin{equation} \mu = \frac{1}{P}\sum_{p=1}^{P}x_p \\ \end{equation}and the sample standard deviation of the inputs $\sigma$ is defined as

\begin{array} \ \sigma = \sqrt{\frac{1}{P}\sum_{p=1}^{P}\left(x_p - \mu \right)^2}. \end{array}- super simple, invertible, and has a profound impact on the shape of our cost function

- lets see what this does to the contours of the cost function we just saw

In [11]:

# show run in both three-dimensions and just the input space via the contour plot

static_plotter.two_input_contour_plot(least_squares_2,[],xmin = -12,xmax = 15,ymin = -5,ymax = 25,num_contours = 7,show_original = False)

- how did the cost function change? lets look at an animation where we slide between the original and standard normalized data

- we will flip through versions of the cost function inputing

where $\lambda$ ranges from $0$ (i.e., we use the original input) to $\lambda = 1$

In [27]:

# animation showing cost function transformation from standard to normalized input

scaling_tool = feature_scaling_tools.Visualizer(x,x_normalized,y,'least_squares')

scaling_tool.animate_transition(num_frames=50,xmin = -12,xmax = 15,ymin = -10,ymax = 30,num_contours = 7)

Out[27]:

- now lets make the same sort of gradient descent run on the normalized input cost

In [13]:

# show run on contour plot

static_plotter.two_input_contour_plot(g,weight_history,xmin = -3,xmax = 10,ymin = -2,ymax = 6,num_contours = 7,show_original = False)

- much much better!

- how about the resulting fit?

In [14]:

# the original data and best fit line learned from our gradient descent run

ind = np.argmin(cost_history)

least_weights = weight_history[ind]

demo.plot_fit(plotting_weights = [least_weights],colors = ['r'],transformer = normalizer)

- not here - to produce the fit we plug in new test points

- new test points need to be treated precisely as the training data - subtract the same mean / divide by the same std

Example 1. Normalizing the input of a student debt dataset¶

- does standard normalization work for real data?

- absolutely - e.g., United States student debt dataset

In [3]:

# load data

csvname = datapath + 'student_debt.csv'

data = np.loadtxt(csvname,delimiter = ',')

x = data[:,:-1].T

y = data[:,-1:]

# plot dataset

demo = regress_plotter.Visualizer(data)

demo.plot_data()

- Least Squares cost before performing standard normalization to input, with run of 25 gradient descent steps

In [4]:

# an implementation of the least squares cost function for linear regression, precisely

# what was shown in Section 8.1 but here pulled in from a backend file

least_squares = cost_lib.choose_cost(x,y,'least_squares')

# run gradient descent to minimize the Least Squares cost for linear regression

g = least_squares; w = np.array([0.0,0.0])[:,np.newaxis]; max_its = 25; alpha_choice = 10**(-7);

weight_history,cost_history = optimizers.gradient_descent(g,alpha_choice,max_its,w)

# show run on contour plot

static_plotter.two_input_contour_plot(g,weight_history,xmin = -0.25,xmax = 0.25,ymin = -0.25,ymax = 0.25,num_contours = 7,show_original = False)

- hugely elliptical! basically impossible to minimize via gradient descent

- because the original input is enormous! so even slight variations from the very best slope/vertical intercept produce huge errors

- corresponding fit will be terrible

In [5]:

# the original data and best fit line learned from our gradient descent run

ind = np.argmin(cost_history)

least_weights = weight_history[ind]

demo.plot_fit(plotting_weights = [least_weights],colors = ['r'])

- after standard normalization, with only $25$ gradient descent steps - with much larger steplength!

In [9]:

# return normalization and inverse normalization functions based on input x

normalizer = standard_normalizer(x)

# normalize input by subtracting off mean and dividing by standard deviation

x_normalized = normalizer(x)

# an implementation of the least squares cost function for linear regression, precisely

# what was shown in Section 8.1 but here pulled in from a backend file

least_squares_2 = cost_lib.choose_cost(x_normalized,y,'least_squares')

# run gradient descent to minimize the Least Squares cost for linear regression

g = least_squares_2; w = np.array([0.0,0.0])[:,np.newaxis]; max_its = 25; alpha_choice = 10**(-1);

weight_history,cost_history = optimizers.gradient_descent(g,alpha_choice,max_its,w)

# show run on contour plot

static_plotter.two_input_contour_plot(g,weight_history,xmin = -1,xmax = 1,ymin = -1,ymax = 1,num_contours = 7,show_original = False,arrows = False)

- way better fit possible

In [10]:

# the original data and best fit line learned from our gradient descent run

ind = np.argmin(cost_history)

least_weights = weight_history[ind]

demo.plot_fit(plotting_weights = [least_weights],colors = ['r'],transformer = normalizer)

8.4.2 Feature scaling for multi-input datasets¶

- the same standard normalization scheme aids in tuning models for multi-innput regression data as well

- simply do the same thing - mean center and scale by standard deviation - for each input

- normalize the $n^{th}$ input dimension of an $N$-input dimensional dataset $\left\{\mathbf{x}_p,y_p\right\}_{p=1}^N$ as

where

\begin{array} \ \mu_n = \frac{1}{P}\sum_{p=1}^{P}x_{p,n} \\ \sigma_n = \sqrt{\frac{1}{P}\sum_{p=1}^{P}\left(x_{p,n} - \mu_n \right)^2} \end{array}- see Section notes for examples!

8.4.3 Summary and discussion¶

- making the contours of a cost function more 'circular' make it easier to minimize - why?

- e.g., for gradient descent due to the nature of the gradient descent direction!

- this direction points orthogonal to contours - in long narrow valleys this points away from cost minimum, on circular cost it points more towards minimum